Technology is supposed to make our lives easier over time, but what is the reality? We may not spend all day hunting and gathering anymore, but we still work similar hours to our great-grandparents. From the paper A Century of Work and Leisure [pdf] published in the American Economic Journal:

We find that hours of work for prime age individuals are essentially unchanged, with the rise in women’s hours fully compensating for the decline in men’s hours. […] Overall, per capita leisure and average annual lifetime leisure increased by only four or five hours per week during the last 100 years.

The following video by CGP Grey called Humans Need Not Apply methodically describes how robotic automation will soon make an additional chunk of people unemployable.

Horses aren’t unemployed now because they got lazy as a species, they’re unemployable. There’s little work a horse can do that do that pays for its housing and hay. And many bright, perfectly capable humans will find themselves the new horse: unemployable through no fault of their own.

If robots are doing all the work, shouldn’t that mean that the workers should be able to get by working less? Some people thought so. The famous economist John Maynard Keynes wrote in 1930 that “by 2030 he expected a system of almost total “technological unemployment” in which we’d need to work as few as 15 hours a week, and that mostly just to avoid losing our minds from all the leisure.”

That is taken from the Vice.com article Who Stole the 4-Hour Workday? (warning: other parts of this site may be considered NSFW), which discusses how the dream of a shortened workweek fell apart:

A new American dream has gradually replaced the old one. Instead of leisure, or thrift, consumption has become a patriotic duty. Corporations can justify anything—from environmental destruction to prison construction—for the sake of inventing more work to do. A liberal arts education, originally meant to prepare people to use their free time wisely, has been repackaged as an expensive and inefficient job-training program. We have stopped imagining, as Keynes thought it so reasonable to do, that our grandchildren might have it easier than ourselves. We hope that they’ll have jobs, maybe even jobs that they like.

The new dream of overwork has taken hold with remarkable tenacity. Hardly anyone talks about expecting or even deserving shorter workdays anymore; the best we can hope for is the perfect job, one that also happens to be our passion. In the dogged, lonely pursuit of it, we don’t bother organizing with our co-workers. We’re made to think so badly of ourselves as to assume that if we had more free time, we’d squander it.

The Vice.com article focuses on the idea that workers should organize and fight for their share of the benefits.

Instead, we see that the benefits of any technological advancement or increase in productivity has predominantly gone to the owning class (business owners, content owners, and corporate executives) as opposed to the working class. A thick, NYT bestselling economics book posits that when the rate of return on capital is greater than the rate of economic growth, the result is wealth inequality.

I certainly don’t know how this will play out. Will robots cause mass unemployment? Will we all have 20-hour workweeks with no pay cut? In the meantime, as an individual its seems wise to keep converting my excess work energy into ownership of assets. If all you do is work, get paid, and spend it all, then you may be stuck in the rat race indefinitely. A way out is to save a portion and buy some assets. Businesses, real estate, shares of common stocks. Or start your own business and/or create some assets.

Motif Investing

Motif Investing

Low-cost index ETF portfolio are everywhere these days! Covestor is a site that usually charges you a fee to manage your portfolio to follow various active managers, with fees ranging up to 2% per year (split Covestor/manager 50/50). However, they recently introduced their

Low-cost index ETF portfolio are everywhere these days! Covestor is a site that usually charges you a fee to manage your portfolio to follow various active managers, with fees ranging up to 2% per year (split Covestor/manager 50/50). However, they recently introduced their  Another online ETF portfolio advisor joins the mix. Discount brokerage

Another online ETF portfolio advisor joins the mix. Discount brokerage

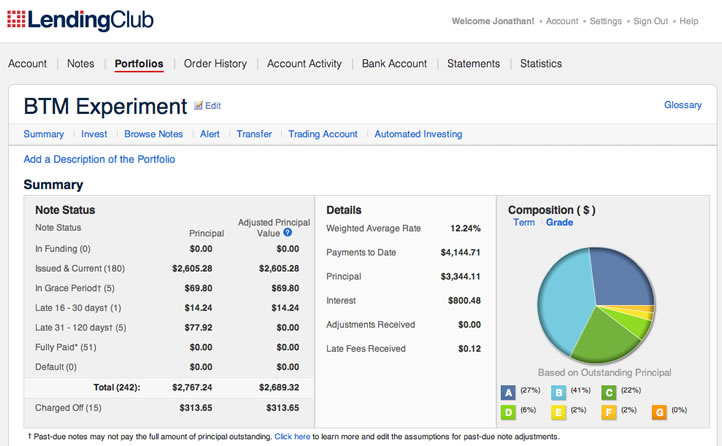

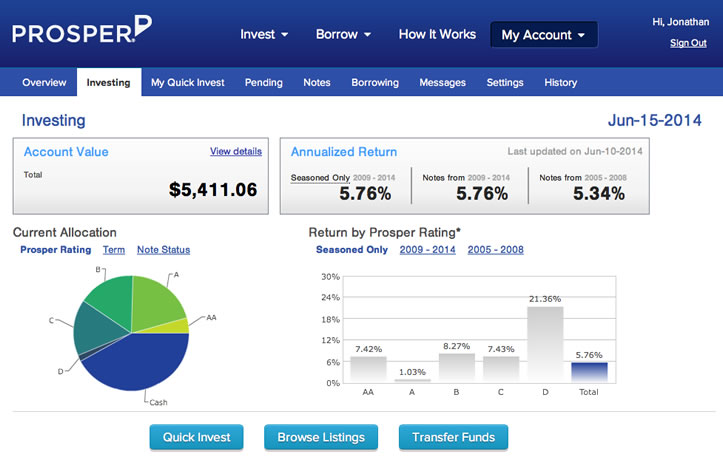

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)