As an iPhone user, I store nearly all of my precious photos on their iCloud service. I used to backup my photos on Google Photos since they offered free unlimited storage at “high” quality, but Google announced it will stop offering this feature on June 1, 2021. After 6/1/21, all photos will count towards your overall storage limit (15 GB free). However, all photos uploaded before 6/1/21 will be grandfathered in and will not be counted towards your storage limit.

As an iPhone user, I store nearly all of my precious photos on their iCloud service. I used to backup my photos on Google Photos since they offered free unlimited storage at “high” quality, but Google announced it will stop offering this feature on June 1, 2021. After 6/1/21, all photos will count towards your overall storage limit (15 GB free). However, all photos uploaded before 6/1/21 will be grandfathered in and will not be counted towards your storage limit.

New iCloud to Google direct transfer tool. This means I have one last chance to make a free backup snapshot of my current iCloud photos. Uploading via app was taking forever, so thankfully Apple just released a new tool that promises to directly transfer all of your iCloud photos over to your Google Photos account. There are some limitations, but here are the directions from Apple Support:

1. Sign in with your Apple ID at privacy.apple.com.

2. Select Transfer a copy of your data.

3. Follow the prompts to complete your request.

iCloud bulk download to local physical drive. In addition, you use the same data privacy tool to download all of your iCloud photos directly onto your computer (or external hard drive) as one huge file. Look for “Get a copy of your data”. It takes them a few days to put it together, but then the download should be much faster than on a photo-by-photo basis. I don’t have enough space to store all my photos on my laptop, but USB flash drives are cheap enough now that I think it’s worth it to create a physical backup copy annually and just leave it in my safe deposit box or safe.

Amazon Prime membership = unlimited cloud photo storage. Something like 2/3rds of all online shoppers have an Amazon Prime membership. If you have an Amazon Prime membership, Amazon Photos will include unlimited photo storage at full resolution. (They only store up to 5 GB of video.)

Amazon Photos offers unlimited, full-resolution photo storage, plus 5 GB video storage for Prime members. All other customers get 5 GB photo and video storage. Securely store, print, and share your favorite photos from the Amazon Photos app. Keep your memories close at hand on devices like Fire TV, Echo Show, and Amazon Fire tablets. Backup your photos to the cloud. Once you save your pics to Amazon Photos you can safely delete them from your device to free up space.

I admit, Apple got me with iCloud and I also pay for their service. I still back them up elsewhere though, as I don’t want to risk losing any sentimental photos. I try to buy discounted Apple gift cards whenever available, and then load them to my Apple account.

An under-the-radar loophole is now out in the open, thanks to fintech app Jiko* publishing a PR release bragging about their

An under-the-radar loophole is now out in the open, thanks to fintech app Jiko* publishing a PR release bragging about their  Here’s my monthly roundup of the best interest rates on cash as of February 2021, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and there are many lesser-known opportunities to improve your yield while still being FDIC-insured or equivalent. Check out my

Here’s my monthly roundup of the best interest rates on cash as of February 2021, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and there are many lesser-known opportunities to improve your yield while still being FDIC-insured or equivalent. Check out my  Walmart+ membership gets you the following perks:

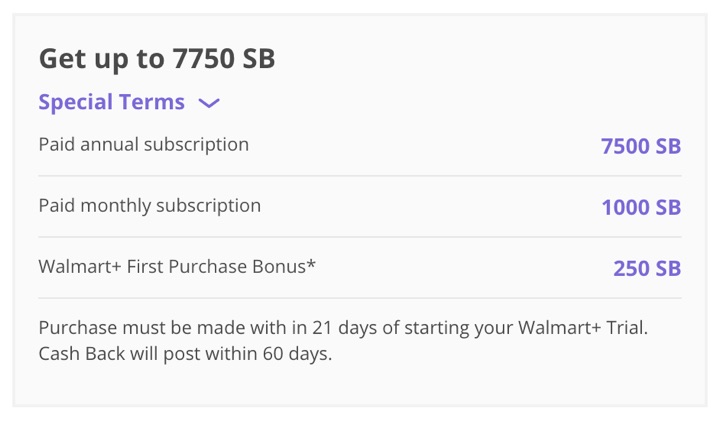

Walmart+ membership gets you the following perks:

While it seems that Robinhood and Gamestop are officially the new gambling version of a multiplayer online video game (

While it seems that Robinhood and Gamestop are officially the new gambling version of a multiplayer online video game (

Alliant Credit Union, one of the top 10 largest US credit unions by assets, has teamed up with Suze Orman to promote their new

Alliant Credit Union, one of the top 10 largest US credit unions by assets, has teamed up with Suze Orman to promote their new  I know I’m a bit late on this, but after reading several media articles, here again is my curated collection of highlights and perhaps overlooked items that might be worthy of additional research.

I know I’m a bit late on this, but after reading several media articles, here again is my curated collection of highlights and perhaps overlooked items that might be worthy of additional research.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

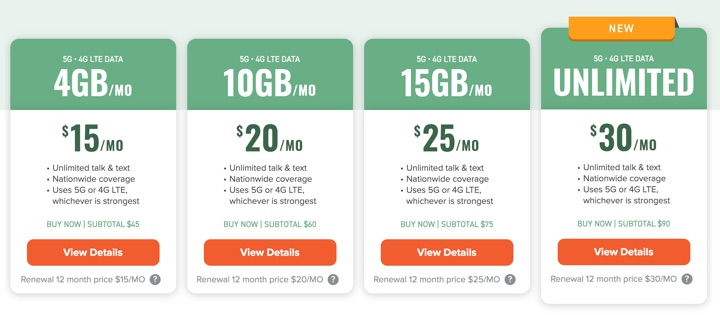

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)