Mastercard has partnered with Instacart to offer a free 2-month membership to Instacart Express when you join with a Mastercard, but after the 2 months you will automatically renew at the $99 annual rate.

Mastercard has partnered with Instacart to offer a free 2-month membership to Instacart Express when you join with a Mastercard, but after the 2 months you will automatically renew at the $99 annual rate.

Join today with Mastercard® to enjoy Instacart Express member benefits for 2 months at no charge. After 2 months, your Instacart Express membership will automatically renew to an annual plan and $99 will be automatically charged to your default, active and registered Mastercard® on file with your Instacart account at the time of renewal. Starting a membership with your Mastercard® updates your default payment method. See your Instacart Express account page to make changes or cancel your plan.

Instacart Express usually costs $9.99 a month and includes free delivery on $35+ orders and reduced service fees. They claim the average savings is $7 per order. Be sure to set a calendar reminder to cancel.

Here’s my monthly roundup of the best interest rates on cash for October 2020, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and also invest in longer-term CDs (often at lesser-known credit unions) when they yield more than bonds. Check out my

Here’s my monthly roundup of the best interest rates on cash for October 2020, roughly sorted from shortest to longest maturities. I track these rates because I keep 12 months of expenses as a cash cushion and also invest in longer-term CDs (often at lesser-known credit unions) when they yield more than bonds. Check out my

If you are an Amazon Prime member, check if you are targeted for a free 30-day trial to Audible Premium Plus which will include

If you are an Amazon Prime member, check if you are targeted for a free 30-day trial to Audible Premium Plus which will include

Mortgage rates have hit another all-time low, with some 30-year fixed rate mortgages below 3% and 15-year fixed below 2.5%. I know that many folks have already refinanced successfully, but these lower rates may offer even more homeowners the ability to lower their payments and/or pay off their home sooner. Importantly, Fannie Mae and Freddie Mac announced an additional 0.5% fee on refinances that was supposed to start on 9/1, but that was just

Mortgage rates have hit another all-time low, with some 30-year fixed rate mortgages below 3% and 15-year fixed below 2.5%. I know that many folks have already refinanced successfully, but these lower rates may offer even more homeowners the ability to lower their payments and/or pay off their home sooner. Importantly, Fannie Mae and Freddie Mac announced an additional 0.5% fee on refinances that was supposed to start on 9/1, but that was just

Walmart is rolling out a membership program

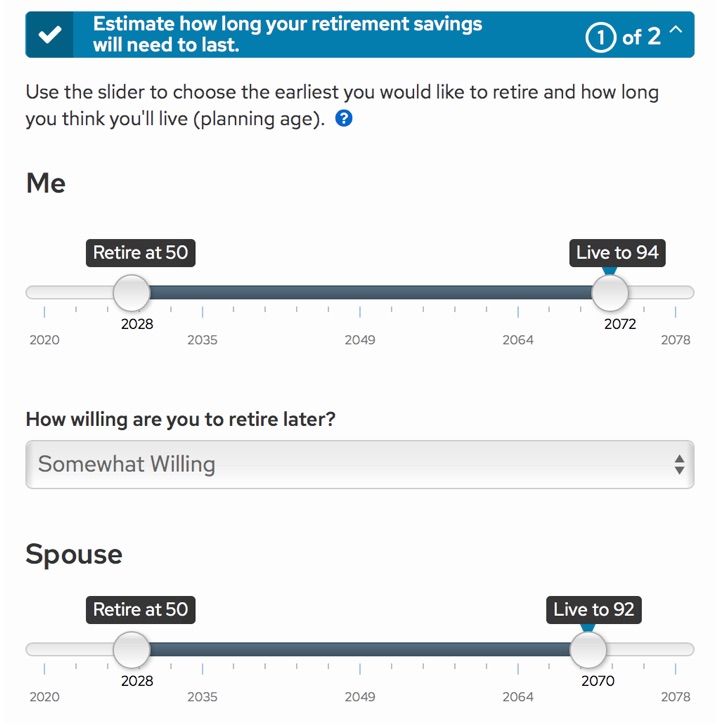

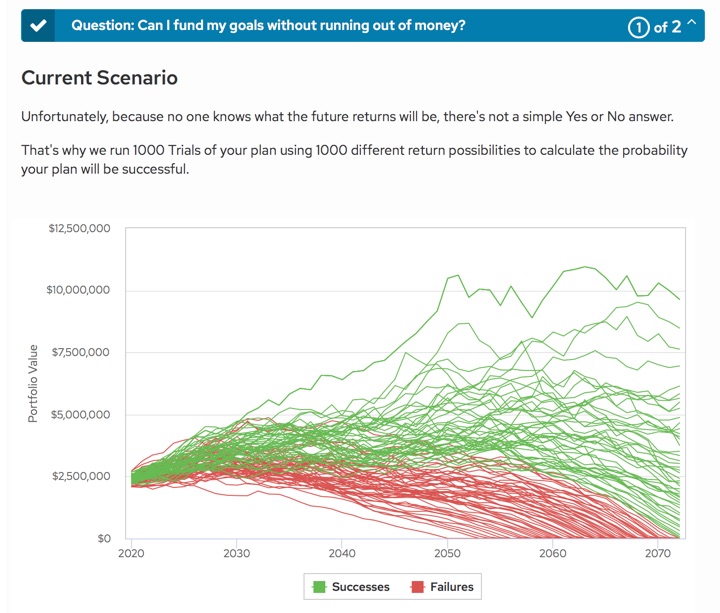

Walmart is rolling out a membership program  Schwab has rolled out a new digital financial planning tool called

Schwab has rolled out a new digital financial planning tool called

Interest rates on liquid savings accounts keep dropping, making bank bonuses more attractive on a relative basis. Opening new accounts are more hassle, so I usually want at least double the interest rates I could get by doing nothing. This

Interest rates on liquid savings accounts keep dropping, making bank bonuses more attractive on a relative basis. Opening new accounts are more hassle, so I usually want at least double the interest rates I could get by doing nothing. This  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)