The Navy Federal Flagship Rewards Card is their “premium” travel rewards card, and it has always had some nice features for those that wanted a single everyday card because it offered a boosted 3X back in travel but also a flat 2X back on everything else. In addition, the points were directly redeemable for cash (not only offsetting past travel purchases).

However, the card also had a $49 annual fee. The sign-up bonus was usually pretty good and included a free year of Amazon Prime membership ($139 value), but it only promised it for a single year. The thing was, there were scattered reports that if you kept the Flagship card linked and charged your next year of Amazon Prime on it, NavyFed would still reimburse you for that second year. But it wasn’t official, and testing it out requires paying for another annual fee, which is a bit risky.

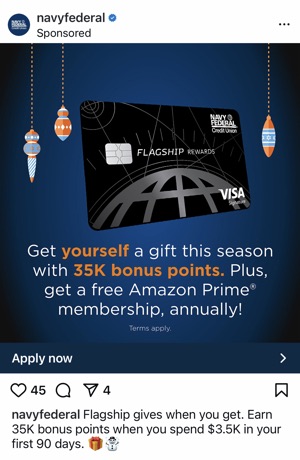

Well, this “secret” perk is finally official! I found this out via an Instagram ad.

I checked and indeed, the application page now says that all cardholders get a “free Amazon Prime® membership (a $139 value, annually)”.

Offer applies only to Amazon® Prime Annual membership that is paid with your Visa Signature® Flagship Rewards Credit Card and posted to your account. Offer is not valid for monthly payment Prime membership options such as Prime Monthly, Prime for Young Adults, and Prime Access. Limit of one Amazon statement credit per Visa Signature® Flagship Rewards Credit Card account, per year. Please allow 6-8 weeks after the Prime Annual membership is paid for the statement credit to post to your account.

The highlights including current sign-up bonus:

- 35,000 bonus points when you spend $3,500 within the first 90 days of opening a new card. 35,000 points is worth $350.

- Free year of Amazon Prime membership. Use the card to purchase an Amazon Prime annual membership, and they’ll reimburse you ($139 value). This now works once a year.

- 3X points per net dollar spent on travel.

- 2X points per net dollar spent on everything else.

- Global Entry or TSA PreCheck fee credit (up to $120), once every 4 years.

- No foreign transaction fees.

- $49 annual fee.

The overall catch here is that in order to apply, you must first become a NavyFed credit union member. Membership eligibility for NavyFed now goes beyond active duty members of the armed forces and DoD employees to include veterans and their immediate family members — including spouses, siblings, parents, children, grandparents and grandchildren.

A smaller catch is that each point is worth $0.01, with a minimum redemption 5,000 points = $50 statement credit. There is a max of $1,500 cash back redeemed each year this way, and you can also redeem 4,900 points to offset the $49 annual fee. Sometimes it gets annoying waiting to reach that $50 threshold. But at 2% cash back on base purchases and 3% back on travel, it’s not a horrible idea to put some purchases on this card. From the fine print:

Visa Signature Flagship cardholders can redeem points for cash (1 point is equal to $0.01). The minimum redemption level is 5,000 points for $50 cash back. The maximum level of redemption is $1,500 cash back, which is equivalent to 150,000 points. Cash back rewards will be credited to your Navy Federal savings account.

I don’t know how NavyFed mathed this one out, but if they keep this structure then this card moves solidly into the “keeper” category for those that already pay for Amazon Prime membership, as the card more than pays for itself each year at $139 vs. $49 annual fee. I also appreciate the straightforward rewards system and $120 towards Global Entry/TSA PreCheck every 4 years.

Side note: NavyFed shares their rules about credit card applications publicly as follows:

Is there a limit on the number of Navy Federal credit card accounts I can open?

Yes. Currently, Navy Federal allows each member to be a primary cardholder on up to 3 Navy Federal credit cards. In addition, we’ll approve only 1 new credit card per member within a 90-day period. This means we’ll decline your application for a new credit card if you opened a credit card within the last 90 days. Note: Home Equity Line Platinum credit cards and GO BIZ® Rewards credit cards aren’t included in this 3-card limit.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)