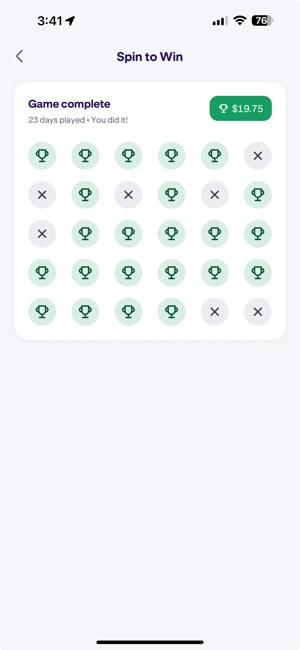

Kraken is best known as a crypto exchange, but as of early 2025 they now offer US stock trading under Kraken Securities through a partnership with Alpaca (press release). They’ve got that VC money and an IPO coming up, so you know that means a high cash burn rate to show high growth! I already saw that with their $75 new crypto account bonus and 30 days of free money spins, where I earned almost $20 in random crypto like DOGE and PEPE:

Until 9/30, Kraken is also offering a 2% ACAT transfer bonus, paid in USDG stablecoin with no cap and 1-year minimum hold period. That’s a pretty solid bonus, with the main concerns being that Kraken is a crypto-first company and there may be some headaches even with SIPC insurance and all that. I’m thinking of moving my US Bank SGOV assets over since they nuked my Smartly 4% card, but I’m a little wary of this brand new brokerage that seems to have been put together by duct tape. In any case, here are the promo highlights.

- 2% bonus on ACAT transfers of stocks/ETFs. No cap. Offer expires 9/30/25. 1-year minimum hold period after 10/1/25.

- The terms indicate you must be Kraken+ subscriber (costs $5 a month or $50 a year) when the bonus is calculated after 1 year, but I’m not sure if they will want you to be a subscriber for the entire year hold period. The language states “Kraken+ subscribers are eligible for a 2% bonus.”, so to be safe I’d probably keep it the entire time.

- Bonus is paid in USDG in , which is Kraken’s dollar stablecoin. If you don’t want to be paid in crypto, it looks like you can sell it to trade, but you can’t withdraw it from the platform until the year is done. I’m not sure how this works in terms of 1099s at the end of the year.

- Kraken Securities will reimburse you for any outbound ACAT fees from your originating broker.

Here’s how I would approach this bonus:

- If I didn’t have a Kraken crypto account yet, I’d open one first and grab this $75 referral bonus.

- For the next 30 days, I’d set a reminder and make sure I open my app and do my daily spin for all 30 days and see if I get a luck $1,000 payout, but probably closer to $15-$30 total.

- In the meantime, I’d sign-up for the 30-day free trial of Kraken+ to sell whatever crypto I didn’t want to keep with much lower transaction fees as a Kraken+ subscriber. This would also prep me for this ACAT bonus.

- I would then quickly transfer whatever I wanted for the this bonus by 9/30. Even if it was just safe SGOV or other T-Bill ETFs, I’d still be getting 2% on top. If I moved $50,000, 2% would be $1,000. Kraken would get nice shiny numbers for their IPO decks. I’d hold for 1 year, making sure I still had Kraken+ on 10/1/26 and then move it to the next bonus.

- Most importantly, I would avoid speculating money on crypto. 2% is a solid guaranteed bonus on top of existing buy and hold assets, but you can easily lose 2% on crypto in a single day and then some!

Here are important excerpts from the fine print:

What is this promotion?

A limited-time incentive offering for eligible U.S. users, providing up to a 2% bonus for qualified transfers of stocks/ETFs into Kraken Securities via ACATS. Kraken+ subscribers are eligible for a 2% bonus. Non Kraken+ users will receive a 1% bonus.Who is eligible?

U.S. residents only, excluding New York and Maine. Users must be fully verified and approved to trade equities. Users must have opened and been approved for a Kraken Securities account.What do I receive if my ACAT qualifies?

You receive up to a 2% bonus (2% for Kraken+ users, 1% for non-Kraken+ users) in USDG based on the value of stocks and ETFs you transfer into Kraken Securities via ACATS during the promo window. The value of the transferred assets is determined at the time the qualified ACAT transfer is successfully completed. The bonus is credited after the promotion period ends and placed on hold for one year (usable for trading but not withdrawable until the hold is lifted).When does the hold period end and how is the hold lifted?

At the end of the one year holding period, which starts on October 1st 2025, the bonus will become eligible for withdrawal provided that the client’s total net transfers into eligible equities remain equal to or greater than the initial value upon which the bonus was calculated.Is there a maximum reward amount I can receive?

No.In what currency will the bonus be paid?

Global Dollar (USDG)Does Kraken reimburse the sender ACATS fees?

Yes. Kraken Securities will reimburse you for any outbound ACAT fees your sending broker may charge you. This reimbursement is not dependent on this promotion and does not have a minimum value requirement to be eligible for reimbursement.

Updated September 2025. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income (

Updated September 2025. That space in your wallet or purse is valuable, and you should be the one to get that value. By being smart and picky, you can find offers worth $500+ for a single card, all to encourage you to apply and try it out. This adds up to thousands of dollars in extra income ( Back again for new NFL season; Everyone must re-enroll. If you are a resident of Washington state and age 18+ (as indicated by your Skymiles account), you can register at

Back again for new NFL season; Everyone must re-enroll. If you are a resident of Washington state and age 18+ (as indicated by your Skymiles account), you can register at

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)