Target date funds (TDFs) get their name because they adjust their portfolio holdings automatically over time based on a given target retirement date. In general, this means shifting from mostly stocks to less stocks over time (known as the “glide path”). TDFs continue to grow in popularity, especially within employer-based plans like 401k’s and 403b’s.

Morningstar Fund Research recently released its 2013 industry survey, Target-Date Series Research Paper [pdf]. While it feels targeted at financial professionals, there are some good nuggets for us individual investors looking to decide where to invest. For example, we have to be careful as look how widely the glide path can very between different brands of target funds:

(click to enlarge)

While the most popular TDF providers have much more similar glide paths, they still differ in important ways (especially after retirement age).

(click to enlarge)

Other highlights from the paper:

Yesterday, I posted a

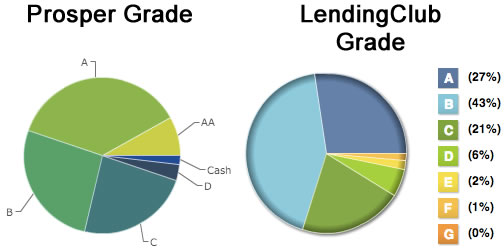

Yesterday, I posted a  I invested $10,000 into person-to-person loans in November 2012, split evenly between

I invested $10,000 into person-to-person loans in November 2012, split evenly between

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

I’ve written about how recent fee disclosure requirements for 401(k) retirement plans have brought a spotlight on

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)